The TSLA Saga Jan 4th

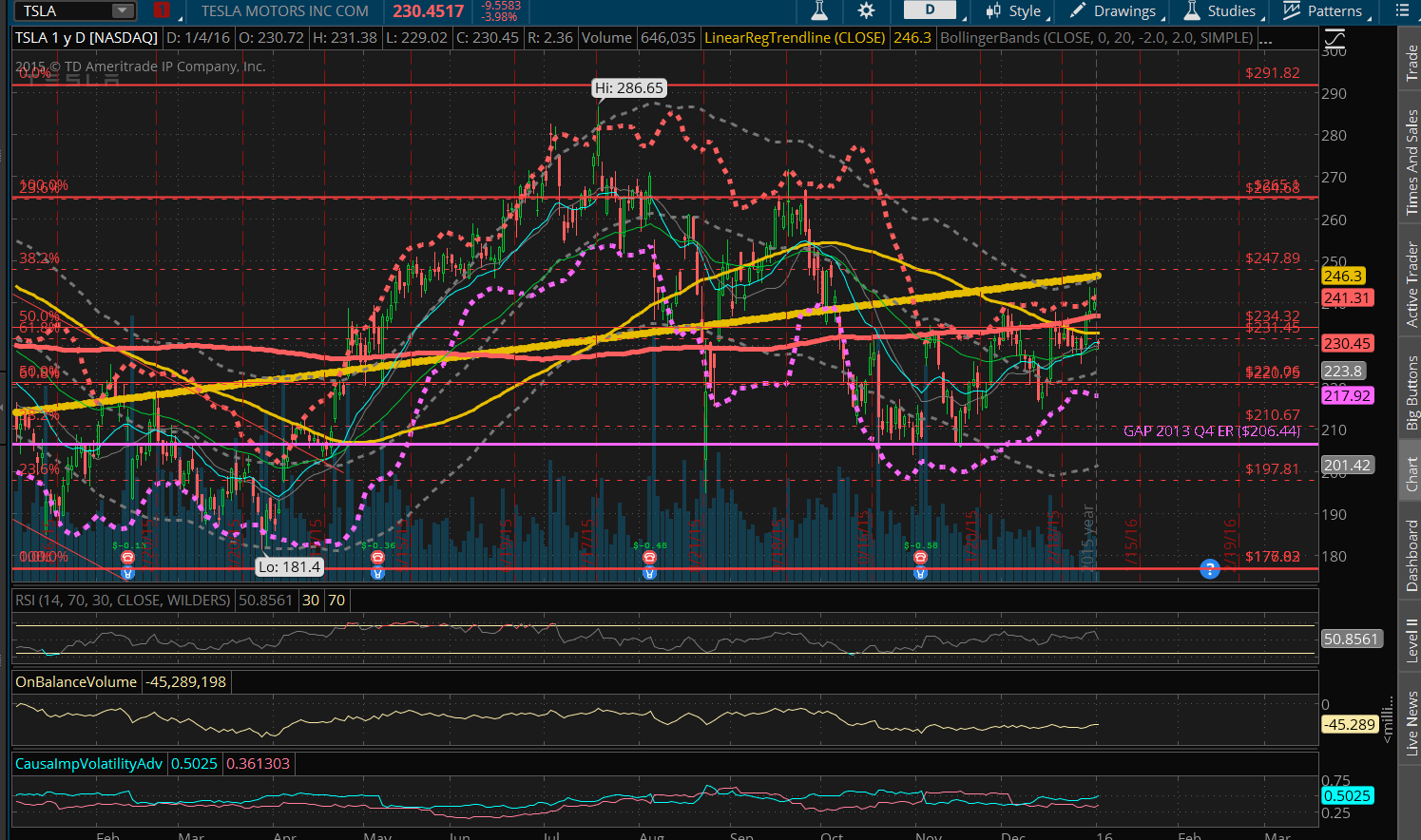

Technical Analysis

Technical Analysis

TA is best for days like this, when you need a prediction of where the potential levels the stock price will stop at. For the downside it will be $220. We are now below the linear regression and the 200 day SMA.

Various news and continued earnings disappointment in the past year have put me in a bad mood with this one. So like George Soros, I clicked sell at the open until my heart feels peace. I will finish the rest of the article later since the stock is experiencing a drop and some might gain some benefit from this.

8 Ball prediction for today is actually worse than when I first looked at it. Before market open. 8 ball says -2%

Fundamentals Stupid

With any stock, there’s always at least two extreme potential outcomes. The only difference between which one is true depends on management’s execution. It’s like Schrödinger’s cat, you don’t know the outcome until proper measurement is made.

From my own brief gut wrenching 2 year stint as CEO, the impression I get is that I was constantly selling a dream. Something that I imagined, but with every execution at each day, a little bit of the dream becomes reality. Then all of a sudden, one event appears to make everything a dream again.

Bad Outcome

That said, TSLA’s fundamentals are slipping and the original rosy pictures is now in doubt. Which makes me ask myself, what is the new picture that no one is thinking about? The pessimist in me says this: “Incredible cash burn for Q4, leaving only 1 quarter of cash reserve. News media is going to have a field day lambasting TSLA as “on the verge of failure”. Which we all know won’t happen, but they will have their pitchfork day anyway. Production will be slower than expected as ramp up will probably just keep pace and not pick up until end of the 1st quarter. Evidence of this is that Elon has been spending most of Q4 at SpaceX sticking the landing. Some kind of hardware refit for Supercharge will need to happen for the fire just to placate the naysayers. There’s no way to say that there’s no fault without losing customer confidence, so the next evil thing is to modify the superchargers instead of recalling all the cars. TSLA energy sees no sales. (Still no news of any sales)

What worries me more is 2017. When Republicans government that is unfriendly to clean tech have a higher chance of getting in power. The more the timeline slip, the more potential of bad government intervention happening during the important Model 3 ramp up.

Good Outcome

They actually manages to ramp up and get cash flow positive in Q1 and meeting expected sales guidance. That’s it. This is how low the bar is set now in order to get a $240 valuation. No need for TSLA energy, no need for Model 3. Just meet these 2 and you get a $240 valuation. Prove that you can execute the production of two models and people will believe your other stories.

Disclaimer

This is a generic disclaimer I attach to all financial based posts to catch all disclaimers. I own everything I talk about. If you suspect I own something or have an Agenda just assume yes. Assume the worst. Assume I am not acting on your best interest.

Leave a Reply